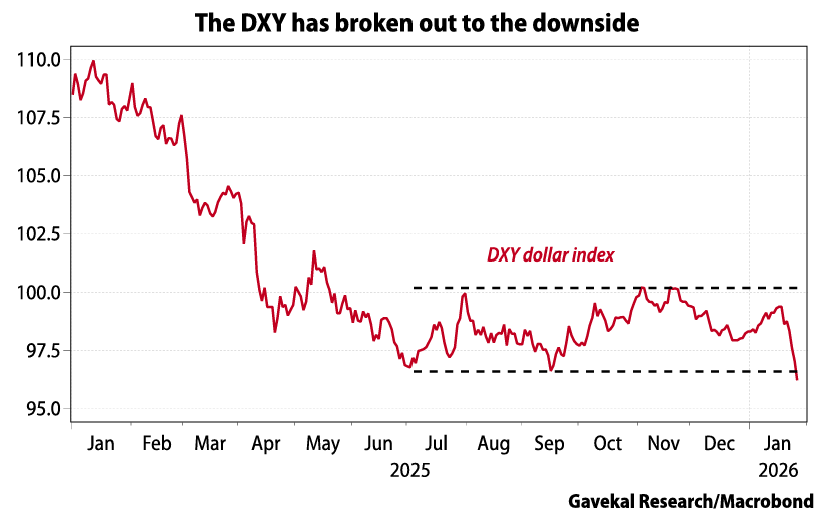

This week we want to address the narrative of a US Dollar collapse. Last year the USD declined from 110 to 98 (an 11% decline in value versus the broad currency basket). This decline has a group of people warning of an imminent collapse in the US Dollar.

We agree that the US Dollar will most likely continue to decline, but do not see the catastrophic collapse forecast by the “Dollar Doom” group.

This graph shows the US Dollar value versus the broad currency basket back to 1967. As you’ll note, there have been several instances when the USD has been significantly lower than today’s exchange rate.

Over the past 20 years, the major driver of USD value has been relative interest rates in the US versus the other major economies.

Between the Global Financial Crisis in 2008 and 2015, the Fed held interest rates at zero leading to a relatively weak USD. For most of this period, the USD traded in the 70s.

Once the Fed began raising rates, the USD value rose as US rates eclipsed foreign interest rates. Between 2016 and the Covid Crisis, USD traded in the 90s.

Post Covid, the Fed restarted its interest rate increases, peaking at over 5% in 2023. This drove a big move higher in the USD as most other countries maintained relatively low interest rates as they tried to recover from the economic damage of Covid.

USD peaked around 110 in 2023 and again in early 2025, but has steadily drifted lower as the Fed has reversed course on rates.

Given the current interest rate outlook in the US versus other major economies, we would expect the USD to retreat back into the 80s. We expect Fed Funds rates to be 3% or lower over the next few years which means the USD is over valued at today’s exchange rate.

This doesn’t mean that the USD is collapsing or that the USD reserve currency status is ending. We believe that this is the normal and historically consistent reaction in currency markets to changes in global interest rates.

Given this view, we remain heavily invested in International Stocks. If USD continues to decline, then this should provide a tailwind to foreign stock returns. It will also enhance US Large Company earnings as over 40% of the S&P 500 profits are earned overseas. As the USD weakens, then foreign earnings get translated to higher USD amounts.

Overall we believe that the gradual decline of the USD is a net positive for investment assets this year.