This week we want to discuss the Venezuelan Oil Industry. Since the US strike on Venezuela, WTI oil prices are up about $2 (3.5%) to $59.70. Some pundits are hailing this latest development as a boon for the US and a major loss for China. We don’t believe that Venezuelan oil is that important to China and don’t expect the US to dramatically improve the oil output from Venezuela.

Oil Reserves

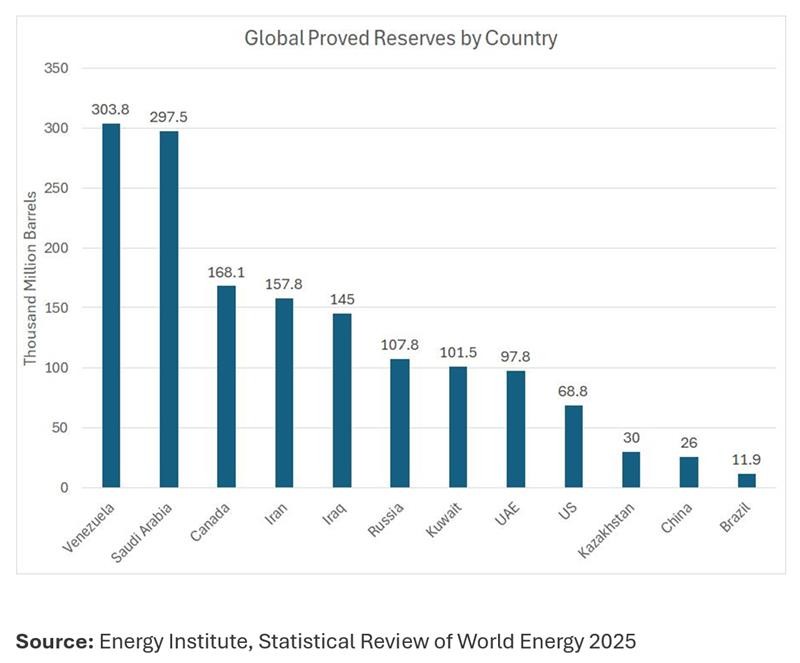

Energy Institute publishes data on oil reserves for producing countries around the world, albeit on an irregular basis, as part of their annual Statistical Review of World Energy.

Here’s the most recent data from their 2025 report, showing oil reserves as of year-end 2020:

At first glance that looks great for Venezuela, right? Well, we have our doubts about the accuracy of these reserve numbers.

Based on Energy Institute data, Venezuelan oil reserves stood at just 80 billion barrels in 2005; in a series of steps, the nation revised its reserve estimates higher to around 300 billion barrels by 2010.

Simply put, these reserve estimates are self-reported by Venezuela’s national oil company, PDVSA, and the upside revisions occurred while Hugo Chavez was President. While PDVSA worked with foreign partners, including Russia’s Rosneft and China’s CNPC, the reclassification of significant extra heavy oil reserves in the Orinoco Belt in the late 2000s as proved reserves was controversial at the time and makes even less sense today at lower oil prices.

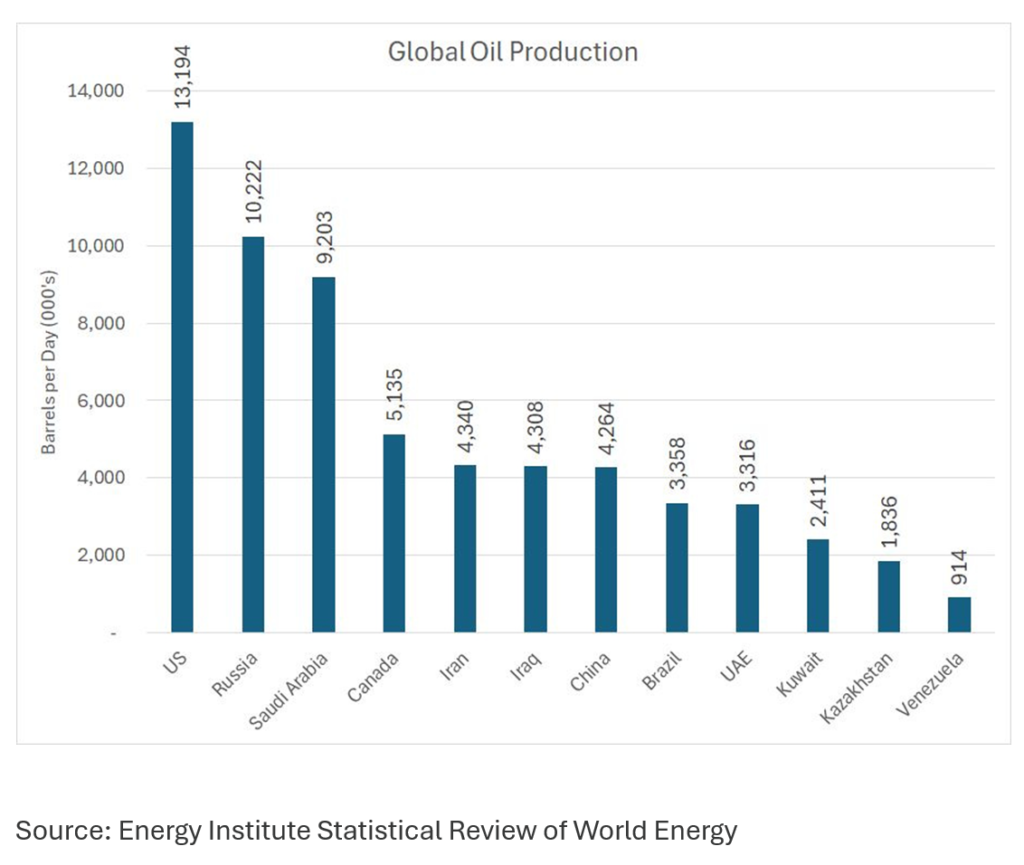

Oil Production

This chart shows annual oil production in thousands of barrels per day for the same dozen oil producers in 2024.

As you can see, there is little relationship between a country’s reserves and its actual rate of production. For example, the USA, which ranks ninth in terms of oil reserves with just 4% of the world total, is by far the world’s largest producer with almost 13.2 million bpd of crude and condensate production in 2024.

Venezuela produces less than 1 million bpd despite the world’s largest reported oil reserves.

Now you might be thinking, “Sure, Venezuela’s low production is just a function of the failed regime.”, however, it might help to understand the nature of Venezuelan oil.

Venezuelan Oil

Most Venezuelan crude is high-sulfur and heavy, making it costly and technically challenging to transport and refine compared with light, sweet grades.

Venezuelan crude has an American Petroleum Institute gravity – or API gravity, which measures petroleum density – of 9.5–12, and sulfur content of 4%–5%, making it comparable to Canada’s oil sands bitumen.

These grades often need to be blended with diluent (such as condensate or naphtha) to make them easier to transport and process. Furthermore, refining such crude also requires specialized refining equipment, like cokers. As a result, these types of heavy, sour crude trade at a material discount compared to international benchmarks.

Based on recent prices for different crude grades and solving for specific gravity, BloombergNEF estimates Venezuela’s heavy crude (that is, without blending) should trade at roughly a $7- to $10-a-barrel discount compared to WTI.

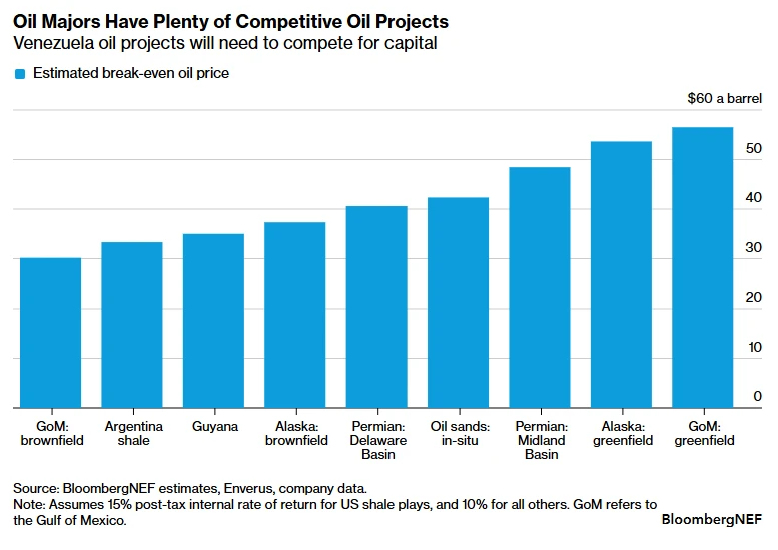

US Investment in Venezuela

We have major doubts about US companies’ desires to invest in Venezuelan oil given their current opportunity set and the break even cost for those plays.

Current estimates for break-even oil price for Venezuelan oil is over $60/bbl. Given the nature of Venezuelan oil, that would translate to a $67-70/bbl WTI oil price.

The majority of US oil production is done in the Texas Permian Basin at a break-even cost of around $40/bbl. Even Gulf of Mexico projects look more economic than Venezuelan oil at present pricing.

Why would US Oil Majors invest billions into an unstable country for potentially decades to produce uneconomic oil?

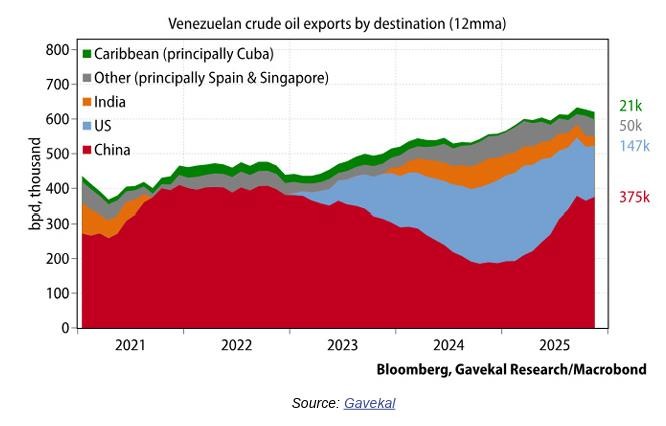

China

So if this isn’t a huge win for the US, it still must be a big loss for China, right?

Well, not really. Politically, it may be a loss for them in relation to having a client state get invaded by an economic and political foe, but China isn’t that reliant on Venezuelan oil for this to be a meaningful economic impact on the country.

Yes, China is Venezuela’s largest oil client, right above the US, but China only purchases about 375,000 bpd from Venezuela.

The EIA estimates that China imports about 11.5 million bpd. So Venezuela accounts for just 3% of Chinese oil imports. China’s major oil suppliers are in the Middle East (Saudi – 1.6mm bpd, Iran – 1.6mm bpd, Other ME – 5.5mm bpd) which account for 75% of oil imports.

Saudi Arabia alone could easily make up the Venezuelan oil shortfall if supplies were cut off from China.

Conclusion

So, the punchline here is that we just don’t see much changing in the oil markets due to the US strike on Venezuela.

US Oil Majors aren’t incentivized to dedicate huge capital resources to poor quality oil fields given their other options and China will easily replace any lost Venezuelan oil.

Once the markets digest the event, we would expect oil prices to return to their pre-strike levels, but we are confident that this isn’t the last volatility event for oil markets in 2026.