This week we wanted to focus on an investment in your portfolio — our position in legacy RMBS.

What exactly are legacy RMBS?

Legacy Residential Mortgage-Backed Securities (RMBS) are bonds backed by pools of residential mortgage loans, where investors receive payments from the principal and interest paid by homeowners on these mortgages. Think of RMBS as simply a passthrough of homeowners’ monthly payments of principal and interest through to the bondholders (i.e. you, the investor).

Legacy RMBS refers more specifically to non-agency deals issued predominately before 2008 (most between 2005–2007). Non-agency means they are not guaranteed by a government-sponsored entity like Fannie Mae or Freddie Mac.

Why do we like this area of the market?

Legacy RMBS pools have borrowers who have weathered the Global Financial Crisis, periods of negative homeownership equity, COVID, and the 2022–2023 rate shock — and are still paying! These borrowers typically have around 60% equity and can therefore withstand very large home price shocks before the investment would be at risk.

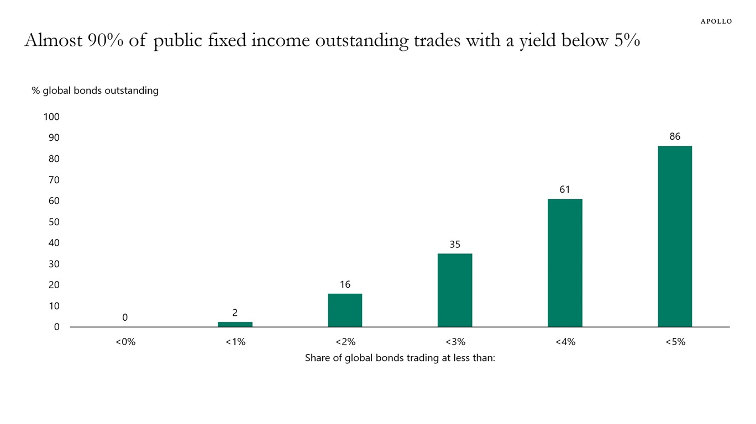

Legacy RMBS exhibits a significant yield premium, and lower correlation, to traditional fixed income investments. These mortgages are paying around 6% while almost 90% of the public fixed income market is yielding below 5%. In addition, the remaining terms on these mortgages are much shorter (now that borrowers are ~ 20 years into paying), which helps reduce risk.

The investment also comes with a unique feature not usually seen in fixed income investments — an ability to do well whether interest rates go up or down:

- When rates rise: Many of the bonds we own have “floating” rates, meaning as interest rates go up, payments to investors increase. These legacy bonds also trade at discounts, which combined with their floating rates, can lead to higher prices when rates rise (something known as negative duration). This is the opposite of what normally happens with bonds, where prices fall as rates rise.

- When rates fall: Normally, mortgage-backed securities underperform other fixed-income investments because of prepayment risk—when interest rates fall, homeowners refinance to lower their payments, and investors are forced to reinvest the returned cash at lower yields. This effect is known as negative convexity. However, in this investment, when rates decline, the discounted bonds we own are paid off more quickly and at full value (par), which typically more than compensates for the usual prepayment risk.

How has the investment has performed thus far?

Since the fund’s inception (10/1/2020) through 9/30/2025, it has delivered a +39.22% cumulative return (6.84% annualized) versus –2.22% (–0.45% annualized) for the Bloomberg U.S. Aggregate Bond Index, with far lower volatility than the overall bond market.

How could this investment suffer?

Legacy RMBS could suffer (as the broader market would), in a scenario of a broad, persistent housing downturn, a sharp rise in unemployment, or a liquidity shock in these markets. We don’t see these scenarios being likely and still expect this investment to hold up well in a mild recessionary environment.

What is the outlook for this investment?

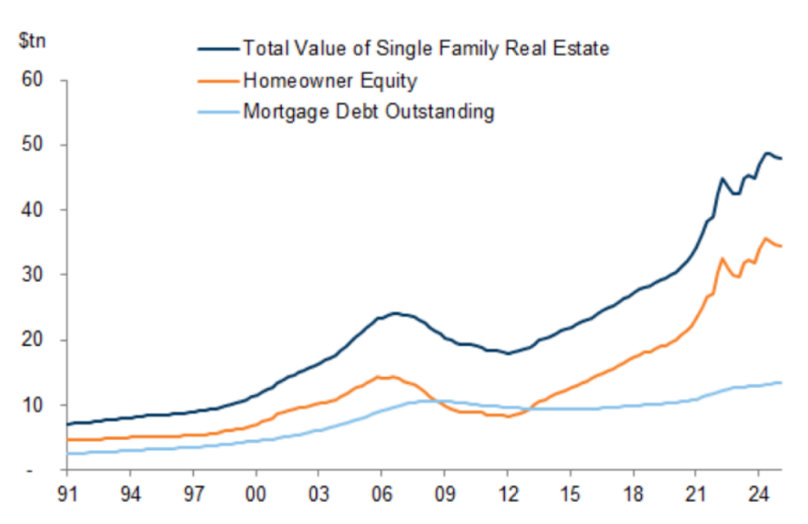

To answer that we want to look at three factors: homeowner equity, mortgage delinquencies, and home prices.

- Homeowner equity: As of June 30, Homeowner equity is at $35.8T which is an important buffer for legacy borrowers and a positive for recovery values in stress.

- Mortgage delinquencies: Mortgage delinquencies remain low (3.93%), which supports credit quality in these legacy pools.

- Home prices: We continue to expect home sales volume and transactions to be slow, but home prices to remain relatively stable (see Weekly Thoughts from 8/22/25 and 7/3/25). Higher home prices should motivate homeowners to make payments, and protect our large loan-to-value buffer.

Conclusion

These data points — strong equity, low delinquencies relative to history, and stable prices — are exactly the fundamentals that matter for legacy RMBS cash flows. With higher yields than traditional core bonds, lower realized volatility, and more moderate correlation to the general bond market, our legacy RMBS allocation remains a higher conviction source of diversified income in a world where the future rate path is uncertain.