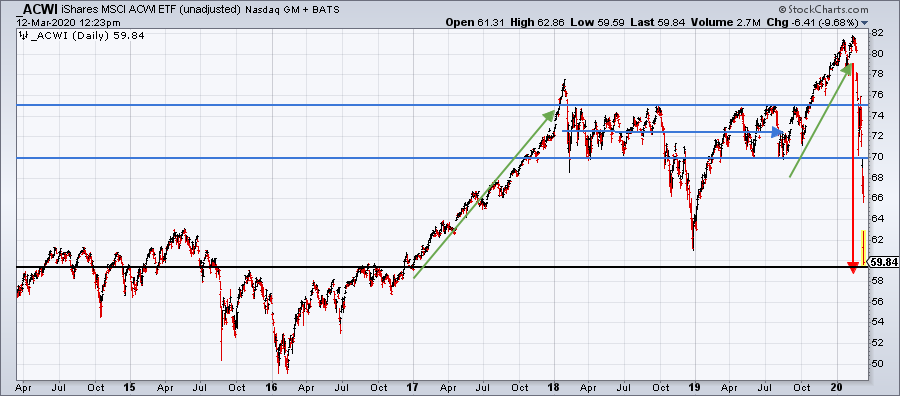

This month has been historic for global financial markets. A combination of extremely high equity valuations in the US, spreading panic due to the coronavirus and an oil price war between Saudi Arabia and Russia have created the fastest market crash in history. The MSCI All World Index has fallen nearly 30% since it peaked on February 13th. We are now back to the levels we saw in the summer of 2014. Yes, you read that right. In one month the market wiped out almost six years of market gains. This is why it is so important to manage risk in the portfolios.

After the first wave of selling, the MSCI All World Index fell back to the bottom of its prior two year range or down about 15%. Historically during a crash, we see a lot of bounces higher. At the end of February the markets were very oversold in the short-term and we got our first bounce. That bounce took the MSCI All World Index back to the top of its prior two year range or down about 7% from the peak. It was at that time that the central banks took their first steps in addressing the decline. The US central bank (The Federal Reserve or Fed) announced an emergency rate cut of 0.5% that we spoke about in last weeks letter.

Our fixed income securities and Treasury Bills have managed to retain their value during the crash. The US Aggregate Bond Index (our fixed income benchmark) is flat since the crash began albeit with a lot of volatility in the past week. Treasury Bills are slightly up over the same period. We have been overweight in both of these markets which has helped us protect capital.

The key to long-term portfolio performance is to minimize the losses in a downturn so that you can buy when asset prices are lower and long-term expected returns are higher.

Our expectations are that global governments will soon have to act aggressively to address market declines and the economic slowdown that is mounting. Over the next few weeks we believe we will see both monetary and fiscal responses to this crisis. First we expect that the Fed will cut interest rates to zero at their next meeting on March 18. In addition, we assume that a new Quantitative Easing program will begin like we saw during the financial crisis where the central bank buys assets thus flooding the world with liquidity. In addition to these monetary policy responses, we expect the Federal Government to act as well. We believe it is likely we see various forms of tax relief for individuals and corporations and potential direct monetary support for critical industries and those that have been negatively impacted by the virus.

Markets tend to panic until the government panics. Meaning stocks will continue to experience severe volatility until government institutions make aggressive moves to intervene in the economy. We think they will do it sooner rather than later. We would expect the markets to rally on this type of news. If we get a normal rally from these levels, we could bounce back up to the prior two year range. However, this crash has been anything but normal so if the markets react badly to a big government intervention then we will need to reassess our current allocations.

As we make allocation decisions we are probability weighting various outcomes to protect capital and preserve growth opportunities. There will come a time again that we will need to buy stocks. Many people just can’t bring themselves to buy when there has been so much carnage but that is when long-term risk adjusted returns are best.