This week we are going to discuss the “End Game” for the Trump tariff policies, but first we’ll provide some context for what is happening in various financial markets.

Financial Markets

The S&P 500 Index is down 17% from its recent peak and down 13% year to date. Over the last three years, it has now delivered just 3.8% annualized returns.

The MSCI World Index is down 15% from its recent peak and down 10% year to date. Over the last three years, it has now delivered 4.2% annualized returns.

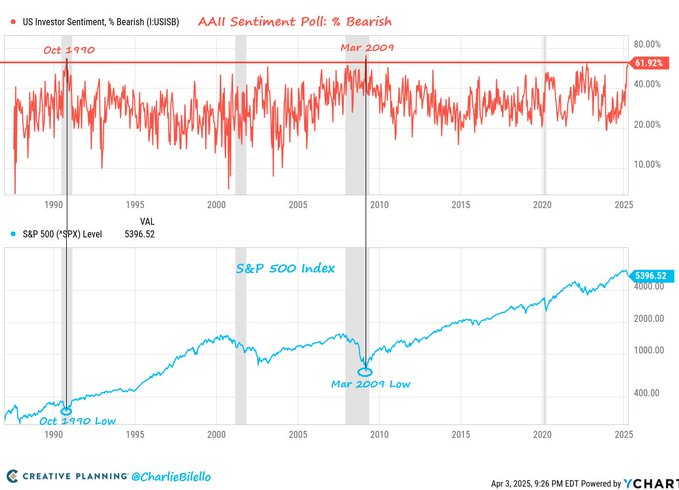

Per the AAII Investor Sentiment Index, investors are now the third most bearish they have been since the late 1980s.

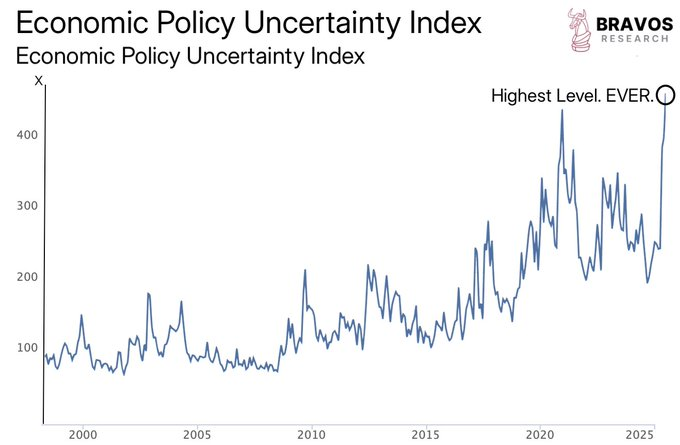

Most of this bearishness is due to the enormous amount of uncertainty surrounding trade policy.

The stock markets are pricing in a global recession but bond markets haven’t yet priced for such a dire scenario. Bond investors may be having trouble balancing the risks of a slowdown in growth and a surge in inflation from the new tariff policies.

The US Aggregate Bond Index is up about 3% year to date but has delivered just 0.8% annualized returns over the last three years.

US 10 Year Treasury Bond Yields have fallen from 4.2% to 4.0% since the beginning of March and High Yield Bond Credit Spreads have increased from 3.0% to 4.0%. So neither of these markets is panicking like the stock markets.

We want to remind everyone that for some time we have been underweight stocks in portfolios due to what we considered higher risk from elevated valuations. On average, portfolios are 10% underweight stocks versus their strategy benchmarks.

In lieu of stocks and public bonds, we have invested heavily in Private Credit markets. This year Private Credit has returned 1% so far with its three year annualized return just above 9%.

We’ll see if Private Credit continues to outperform, but we believe the current level of volatility in public markets is creating opportunities for long-term investors.

To understand what comes next in markets, it is critical to understand the core goals of the administration with their tariff policy.

New Tariffs

President Trump’s tariff announcement this week seemed to catch everyone off guard. Consensus was that they were much larger and more esoteric than expected. In addition to the enormous scale, many questioned the methodology of selecting these “reciprocal tariffs”.

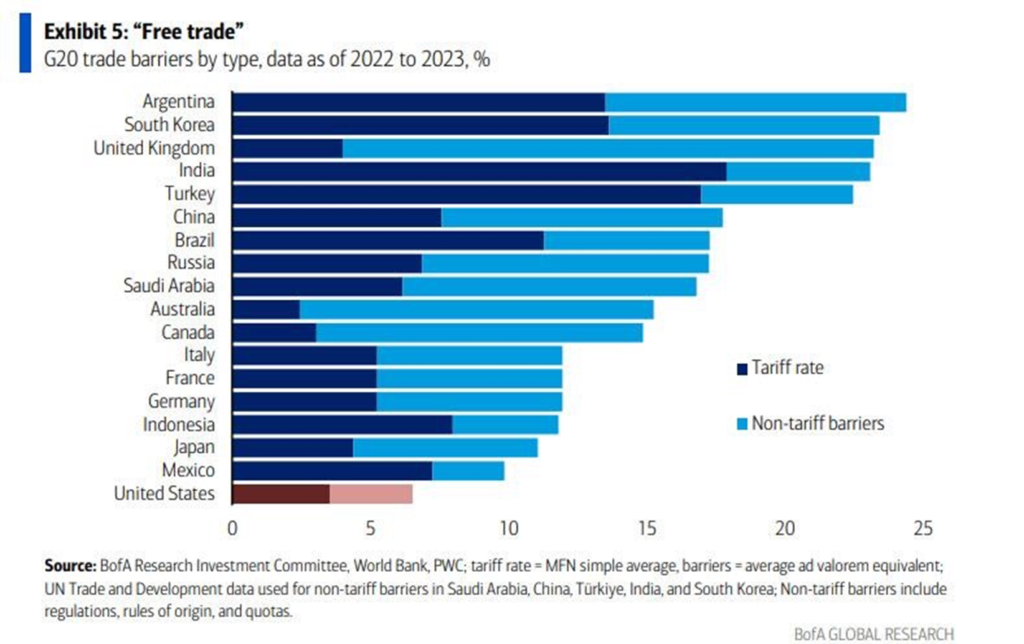

Wall Street was expecting the administration to reference the existing tariff and trade barriers of other countries (see above) and then match them. But it appears that the administration chose to focus on the trade deficits the US has with each country and then apply a tariff of half of that deficit amount. Obviously, this shocked the markets.

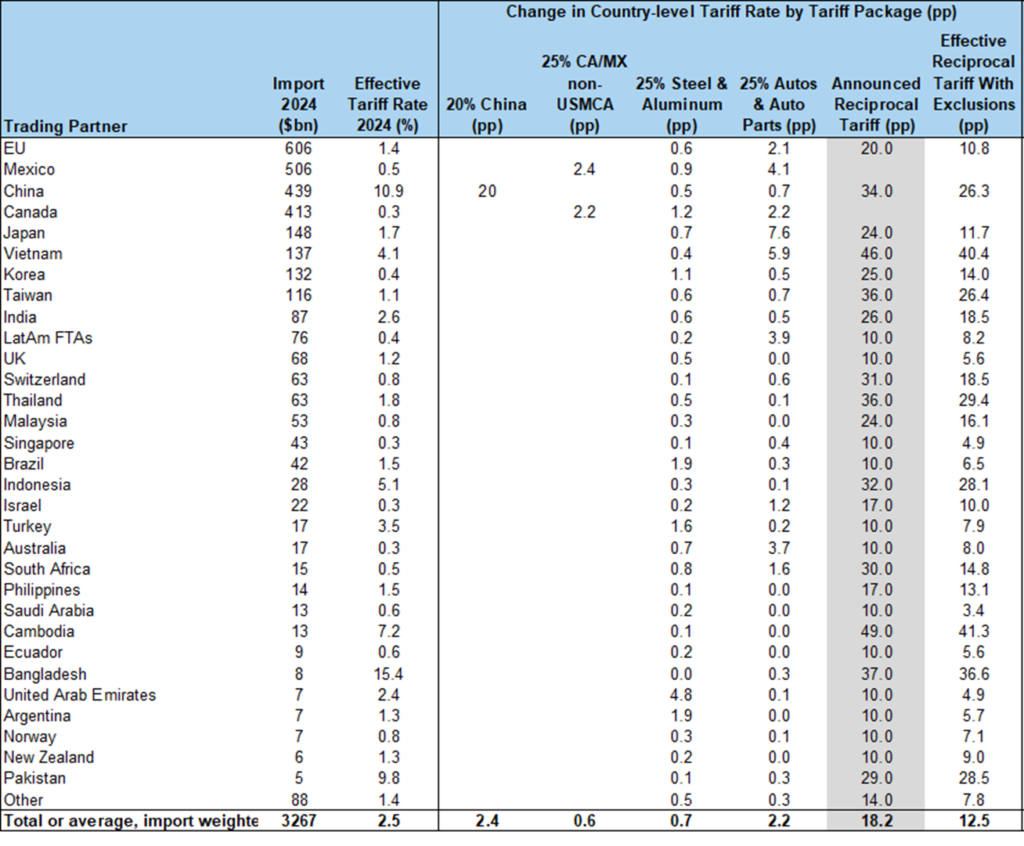

We’ve seen many estimates of the total tariff burden under this new program with some claiming we are now at levels last seen in the depression. However, the detailed analysis above from Goldman Sachs shows that if the current tariff program remains as is, we will have an effective tariff rate of 12.5%. The last time tariffs were this high in the US was at the end of the 1940s.

The End Game

The trillion dollar question is now—What are they trying to achieve with this program? We believe it is likely one of or a combination of three goals.

- Decoupling

- Funding

- Negotiating

Decoupling

We call an attempt to alter global supply chains and restore US manufacturing dominance, decoupling. This would entail separating the US economy from the current manufacturing hubs and forcing companies to make their products domestically regardless of the impact to prices or profit margins.

The perceived benefits of this goal would be:

- Improved national security

- Additional jobs and increased wages

- Expanded domestic tax base

If this is their core objective then we might be in for a very long and painful adjustment.

To accomplish this outcome, the tariffs would need to remain indefinitely, forcing companies to invest enormous amounts of capital in new manufacturing facilities in the US. We would expect to see a large one-time jump in the prices of many products and a hit to corporate profit margins.

Deutsche Bank estimates that the current tariffs would reduce GDP growth by 1.5% annually and Goldman Sachs thinks that earnings growth would be reduced by 6-8% if the tariffs remain.

The likelihood of these policies actually achieving the perceived benefits is pretty low given the enormous cost difference between US Labor and the rest of the world.

This scenario would most likely cause a global recession. The stock markets appear to think this is the ultimate goal of the administration.

Funding

We call an attempt to establish a new source of government revenue and to refinance the national debt at lower rates, funding.

Trump has talked several times about how much the country would benefit from tariff revenues. Current imports into the US are $4 trillion. Applying the Goldman Sachs effective tariff rate to this would imply a $500 billion per year tax on trade. This would be about 21% of the current income taxes received by the federal government.

However, if the current tariff rates were to remain, most economists estimate that imports would collapse offsetting most of the revenue gains. A more sustainable rate would be 5% (still double from the prior rate) leading to $200 billion in annual tariff revenues.

This tariff revenue would most likely be “rebated” to taxpayers in the form of lower income tax rates.

In addition to establishing a larger tariff revenue stream, the administration might be using the current uncertainty for force interest rates lower. Trump has talked about how unsustainable the current national debt interest payment is and this might be a way to reduce it.

The current weighted average interest on the national debt is 3.3%. Just 17% of that debt matures beyond 20 years and 22% matures in the next year. If the administration could create enough fear to force US Treasury Yields lower, they might be able to refinance the debt at lower rates and longer maturities.

If they were able to reduce the weighted average interest rate by 1% this would save taxpayers about $400 billion per year at current debt levels.

If this is their ultimate goal, we don’t think that they will be successful with refinancing the national debt at rates that would be meaningfully lower unless they are willing to crash the economy (not our base case). We do think that they will maintain effective tariff rates in the 3-5% range in order to pay for income tax cuts.

Negotiating

We call an attempt to use the new tariff program as leverage to change existing tariffs and trade barriers on the US, negotiating.

As you saw in the existing tariff and trade barrier graph above, there are significant penalties on US exports. If the US could convince its major trading partners to allow free trade on US goods, then this would be a huge win for the global economy and US companies.

We believe that this is the core goal of the administration’s new tariff program. We aren’t sure how long this might take, but many of our trading partners are much less equipped to endure the economic chaos of these tariffs than the US.

If the administration is successful with this goal, we would expect to see improved corporate profits and expanded export volumes.

If we are right and the new tariffs start to be removed as our trading partners renegotiate bilateral trade, then we would expect investor sentiment to quickly reverse and stock prices to rise.

We are presently waiting for a bit more clarity on this before we adjust our current underweight positioning.

Is the New Tariff Program Legal?

Regardless of their ultimate goal, many are now questioning if the President has the power to unilaterally change tariff policy.

The newly announced reciprocal tariffs invoke the authority of the International Emergency Economic Powers Act (IEEPA), the National Emergencies Act and the Trade Act of 1974, based on a declared emergency related to “large and persistent annual U.S. goods trade deficits.” Other tariffs have been implemented with a stated intent of combatting emergencies related to illegal immigration and illicit drugs. Using these measures to impose tariffs is unprecedented and will likely face legal challenges.

Per Peter Boockvar:

The lawsuits are now coming for the administration over tariffs on the basis that there is no National Emergency that is being claimed that would empower the President to implement such tariffs.

According to a Reuters story, the “New Civil Liberties Alliance, a conservative legal group, on Thursday filed what it said was the first lawsuit seeking to block Donald Trump’s tariffs on Chinese imports, saying the US president overstepped his authority.”

Trump has used the International Emergency Economic Powers Act of 1977 as his legal basis.

Andrew Morris a senior litigation counsel member of the NCLA said in a statement, “By invoking emergency power to impose an across-the-board tariff on imports from China that the statute does not authorize, President Trump has misused that power, usurped Congress’s right to control tariffs, and upset the Constitution’s separation of powers.”

The lawsuit was filed on behalf of Simplified which is a Florida based retailer of “home management products.” And, “The lawsuit says presidents can only impose tariffs with Congress’ permission and under complex trade statutes spelling out how and when they can be authorized.”

We should expect a lot more of this as there is no emergency that would precipitate what is going on. I only went to law school for one year but it seems pretty obvious. It could end up being the courts over the next week that freeze what is going on rather than the result of trade negotiations.

We expect that we are near peak uncertainty around this topic. Hopefully, investors will begin to get more clarity on the purposes and legality of this new tariff program in the coming weeks.