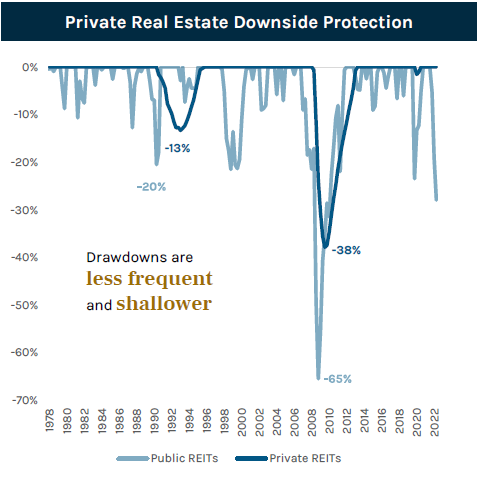

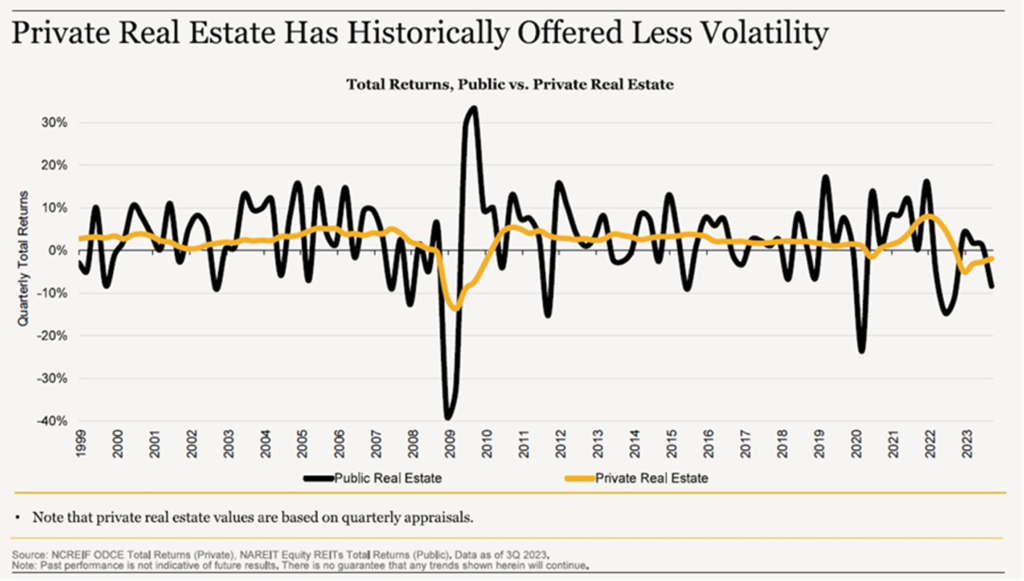

Invitation Homes (INVH) is a public real estate company that owns over 5,000 residential homes across the US. In early 2020, the company’s value declined over 50% only to recover most of this value a few months later. The actual median sales price of homes sold across the US was starting to climb during this same time period. Did all 5,000 homes lose half of their value and then recover it a few months later?

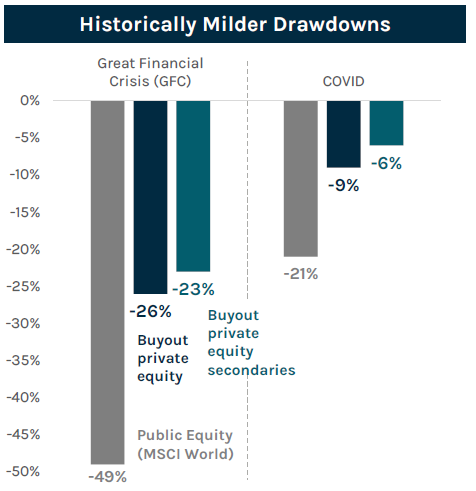

The lower price volatility of private investments is an appealing characteristic for investors tired of the whiplash sometimes experienced in public markets. Volatility is just one form of risk and while private investments often provide investors with a smoother ride, there are many other risks you need to consider before making a private (or public) investment. Academics frequently debate whether public investment pricing or private investment pricing is more accurate. Private investment managers accuse public investments of “excess volatility” and public investment managers accuse private investments of “volatility laundering”. We see the merit in both sides of this argument and believe the truth is somewhere in the gray area in between.

Common Misconception: The Illiquidity of Private Investments Is Not Appropriate for Individual Investors

Private investments are less liquid than public investments and this illiquidity is a risk. All investments have risk and the return you receive for holding that investment generally corresponds to the risk you accept.

We call the higher return you receive from this illiquidity the “illiquidity risk premium”.

The Yale Endowment has an infinite time horizon and can support allocating over 75% to alternative investments because they can accept this illiquidity (and receive the higher return).

Our clients don’t live forever, unfortunately, but do you really need 100% of your retirement portfolio available for withdrawal every day? Most research on this topic actually concludes that the average investor fails to properly capture this increased return by not accepting enough illiquidity (see a recent CFA article here).

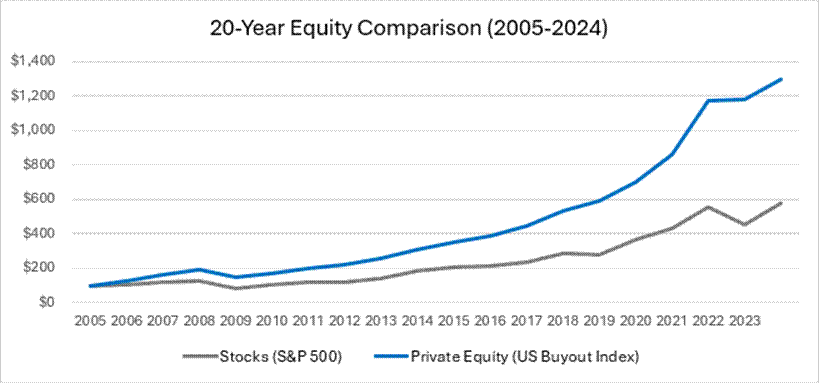

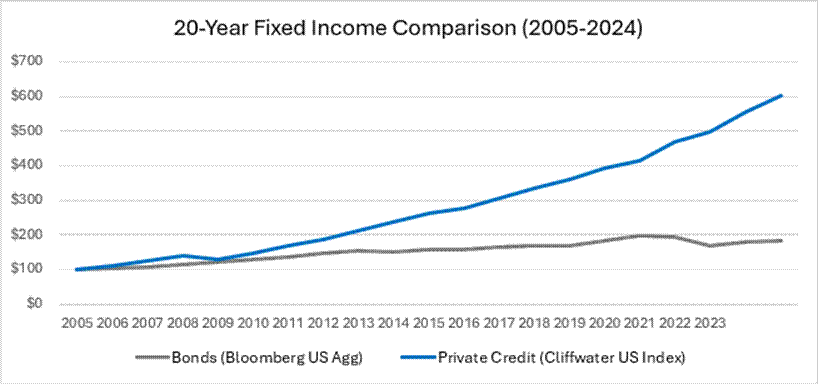

The actual amount of additional return you receive from this illiquidity varies across time, market cycles, and investments. Here is Bloomberg’s attempt to calculate the illiquidity risk premium in private equity:

Private investment managers recognize that locking up funds for 10+ years may not be appropriate for some individual investors so many have created funds that offer quarterly redemptions.

Remember that these private investment funds mostly hold long-term investments so they must install safety guards to protect against a forced fire sale scenario so these quarterly redemptions can be restricted in certain environments.

It is important to fully understand the illiquid nature of the underlying fund assets, the redemption provisions allowed by the fund, and how these dynamics may interact in various environments. The illiquidity of private investments needs to be carefully evaluated in the context of an investor’s possible future cash needs and potential opportunity costs but, in general, most investors should allocate more to less liquid investments and better capture this illiquidity risk premium.

Common Misconception: All Advisors Can Access the Same Private Investments

The private investment landscape is evolving rapidly allowing more access for individual investors and we are confident this trend will continue. However, the access to these various private investment strategies varies widely by advisor and platform.

The large wirehouse firms (Merrill Lynch, Morgan Stanley, Wells Fargo, UBS, etc.) only allow a fraction of the private investment offerings onto their platforms. Often, they require those private investment managers to pay a significant fee to be on the platform (“pay to play”).

Many private investment vehicles offer the same private investment fund in different share classes allowing the advisor and wirehouse to collect fees in different ways. As a fee-only advisor, we never earn a sales commission for any investments we make.

We were researching a private real estate fund last year that we decided not to invest in but it highlights the importance of how you choose to access private investments.

We could invest in the fund through the institutional channel at a 14% lower cost and lower ongoing expenses than the exact same fund offered on Morgan Stanley’s platform resulting in an estimated 42% better return (using the fund’s base case return projections over 5 years).

Also, many of the private investment managers completely avoid the wirehouse firms and choose to partner with only a select number of advisors. Being an independent RIA with private investment expertise, we can access a broader menu of private investments than most advisors.

We’ve covered a lot of ground yet have only scratched the surface on private investing. This new evolution of private investments is an exciting time allowing individual investors access through advisors to a private investment world that was previous restricted to large institutions and the ultra-high net worth investor.

However, private investments can be complex and most advisors do not have adequate expertise to analyze these investments. We do agree with the WSJ author’s concern over this movement, “There’s a dark side: encouraging financial advisers and investors to believe that anyone can easily mix private funds with public assets.”