The Global Stock Markets regained all-time high levels this week. In just a little over two and a half months, investors have gone from utter fear and panic, pushing markets down 20% to euphoria and new record levels.

Just another in a long list of such examples, that it doesn’t pay to invest based on emotion. So instead of yet another note on the madness of markets, today we want to talk about the numbers.

Stock market prices represent the present value of many years of future earnings. These future earnings get discounted to a current value based on prevailing interest rates and earnings growth. Many on Wall Street use an abbreviated methodology to assess the current prices—Price to Forward 12 Month Earnings. While it’s a cheat vs more in-depth analysis, it can provide insight into the relative value of different stocks.

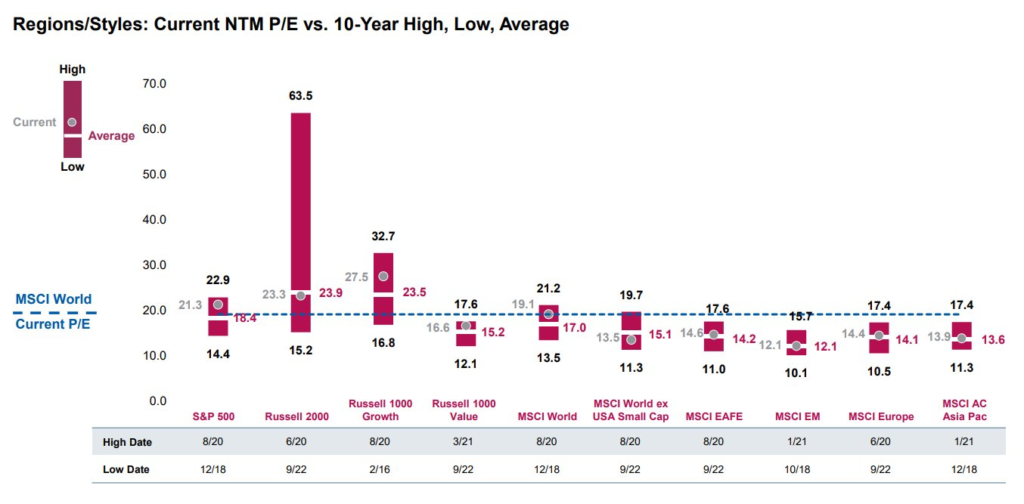

The graphic above is a bit of an eye chart, but it shows the current NTM P/E for many of the major global stock markets and their historical valuation levels.

The Global Stock Market (MSCI World) is trading at 19x NTM Earnings vs its average over the last decade of 17x—a 12% premium.

Digging into the components of this index, we quickly see that the MSCI World Excluding the US is trading at a discount of 11% relative to its 10 Year Average NTM P/E.

The US S&P 500 Index is trading at 21.3x vs its average of 18.4x or a 16% premium. Without understanding the causes of this valuation shift, some investors are convinced that US stocks should be sold as they are clearly overvalued. But is that really true?

Ms. Subramanian at Bank of America recently released a research note on this very topic, which we find very illuminating. She notes that the historical composition of the S&P 500 has changed dramatically and is now a much better basket of stocks than it used to be.

She cites the following as reason that justify the current premium valuation relative to history in the US Large Cap Market:

- The US companies are half as indebted as other global regions

- Earnings volatility in the US is much lower than in Europe

- Free Cash Flow per share is higher in the US than in Europe or Asia

- The Percentage of non-profitable companies is lower in the US

- Earnings Forecast dispersion is tighter in the US reflecting greater transparency

These are all solid reasons that US Stocks should trade at a premium to other markets and to their historical averages. We would also add earnings growth as well.

Expected S&P 500 earnings growth is currently forecast at 9.2%. This is much better than Asian growth at 7.5% and Europe at 3.4%.

So while the US Stock Market may appear to be a bit overvalued, we think there are a lot of good reasons to own these stocks. We continue to have a large allocation to the US and to Tech/Telecom in particular.

This isn’t to say that we will be exiting our International Stock holdings. We still think that they are attractively valued and have significantly outperformed this year, up over 18% vs 4% for the S&P 500.

However, with the markets now at new all-time highs, we wouldn’t be surprised if investors start to take some gains in the short-term based on emotion.