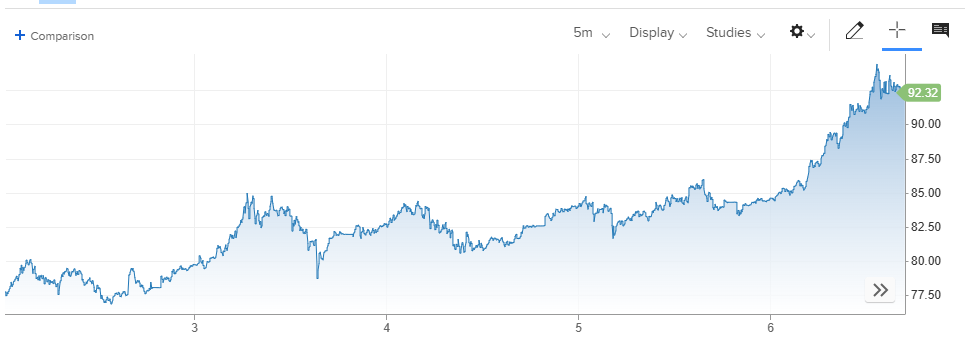

This week we’ll address the elephant in the room – Iran. As we predicted last week, the US attack on Iran has produced a lot of volatility with a corresponding surge in oil prices. US stock market volatility increased by almost 30% this week and Brent Oil prices have increased 21%.

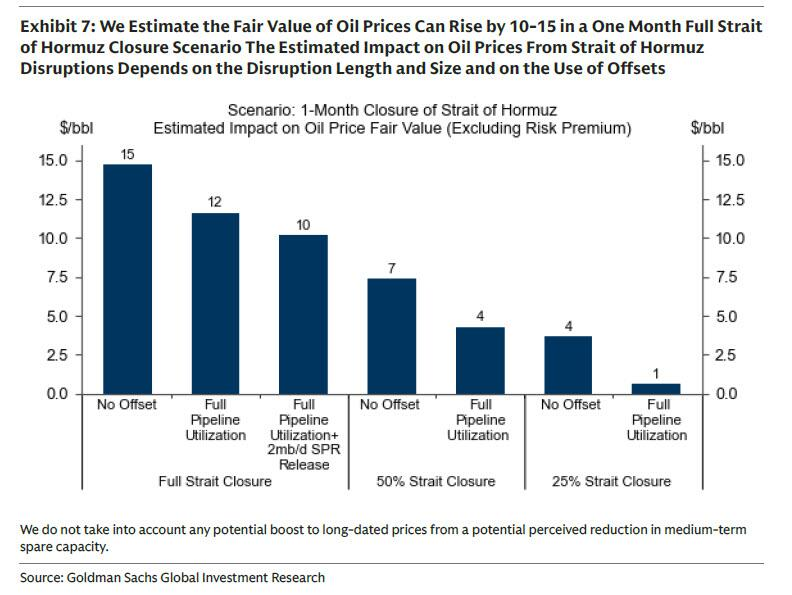

On Sunday night, Goldman Sachs estimated that a one month closure of the Strait of Hormuz would result in a $15/bbl increase in the price of oil. That’s exactly the price increase we saw this week, so markets are pricing in at least a four week pause on oil shipments from the Persian Gulf.

While US stocks had a bumpy ride this week due to increased volatility, overall the impact of the Iran attacks has been muted. The S&P 500 is down just 1.5% since the air strikes began.

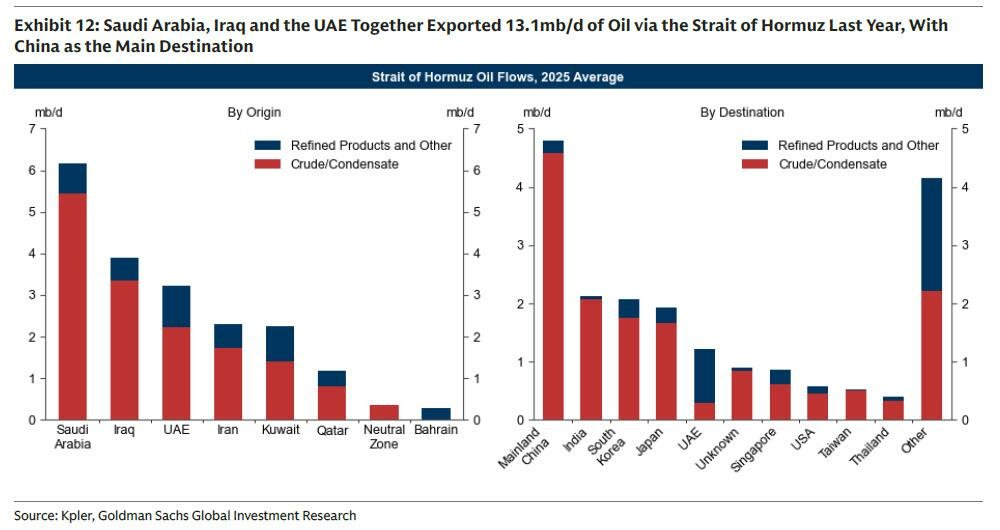

International Developed Country stock markets dropped 5.6% this week with the major Asian markets falling by nearly 7%. Countries with a larger exposure to Middle Eastern energy supplies were punished in this week’s trading.

As you can see from the graphic above, China, India, South Korea and Japan are the largest recipients of oil and refined products from the Persian Gulf.

If the conflict in Iran lasts too long their economies will become increasingly impaired by the lack of oil exports from the region.

The Trump administration is beginning to take steps to prevent this scenario by ordering US Navy ships to escort oil tankers through the Strait of Hormuz and by providing up to $20 Billion in reinsurance funding. We’ll see if these programs provide relief.

Usually during an event like the current conflict in Iran, investors would move funds into US Treasury Bonds in what is called a “Flight to Safety”. This week that didn’t occur. US 10 Year Treasury Bond yields actually rose by 0.17% as bond prices fell.

This is very abnormal for this type of situation, but the cause may be investors’ changing views on inflation due to the oil price spike.

Based on current oil and gasoline prices, March’s CPI number could be 0.35% higher than it otherwise would have been.

Echoing this rationale, the Fed Funds Futures adjusted this week forecasting a much lower likelihood of an interest rate cut this summer.

Obviously, there are a lot of moving parts right now on the investment landscape. We are cautiously optimistic that once the current conflict ends financial markets will refocus on positive earnings and economics.