Over the last ten days, the stock market has rallied on hopes of a quick end to the Iran conflict and optimism that the Federal Reserve will cut interest rates as expected in spite of rising inflation due to higher oil prices.

Since March 30th, the S&P 500 is up 7.5% and is now down just 0.4% year to date. International Developed Market Stocks are up over 9% over the same period and have returned 8.3% year to date.

While there are a lot of things that could go wrong in the Middle East over the next few months, for now, investors are choosing to refocus on corporate earnings growth and valuations.

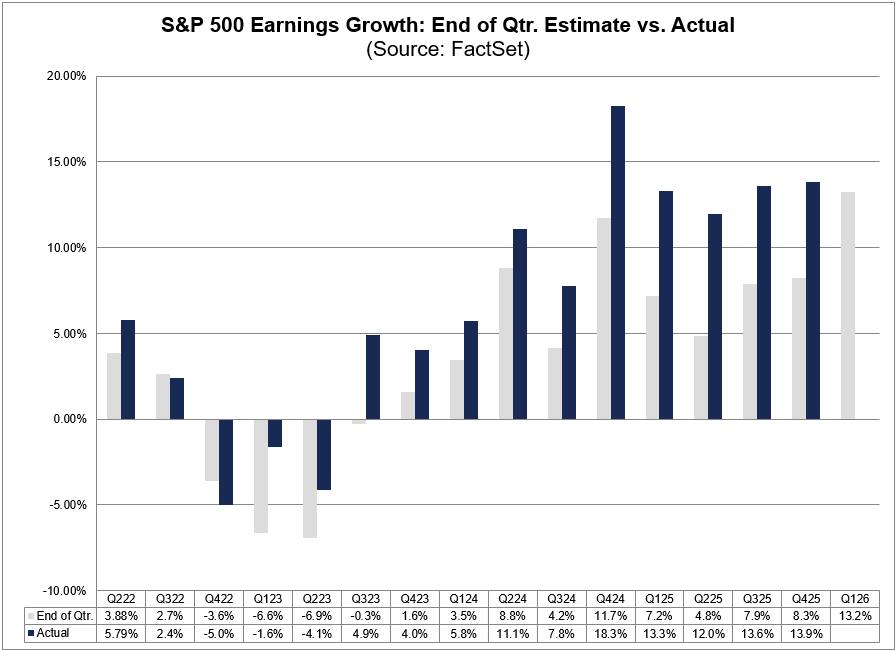

The companies that constitute the S&P 500 are expected to grow earnings in Q1 2026 by 13.2%. Based on the recent trend of earnings growth beats, FactSet estimates that earnings growth could come in between 18-19% in the first quarter.

Of the expected 13.2% earnings growth, the bulk of that growth is forecasted to come from the Technology Sector. The latest estimate is for Tech earnings growth to come in at 45% in the quarter.

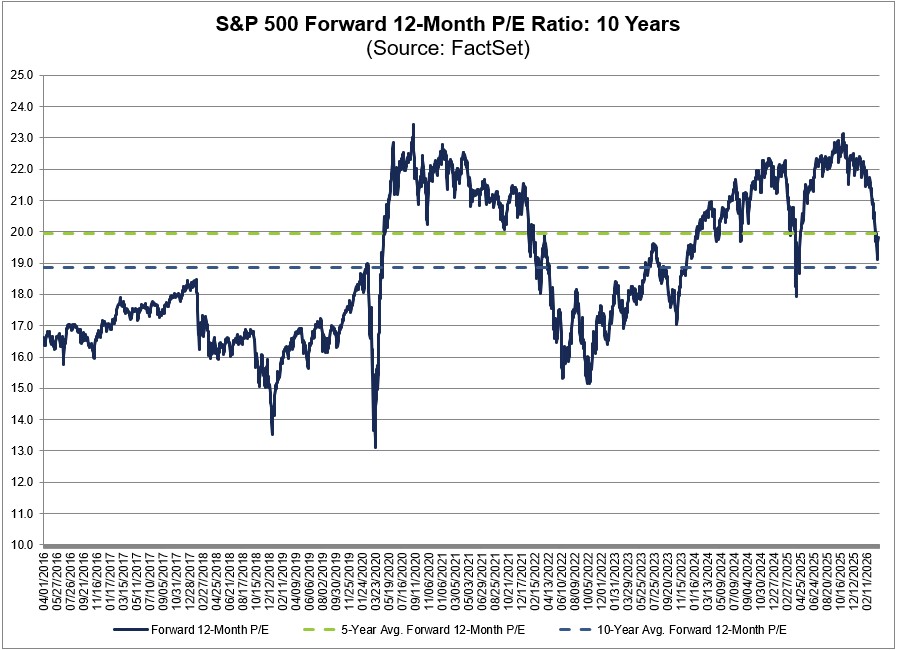

This very strong earnings growth combined with the recent pullback in stock prices have combined to push valuations to quite reasonable levels.

The 12 month forward P/E multiple for the S&P 500 is now just 19x, very close to the average level of the last decade.

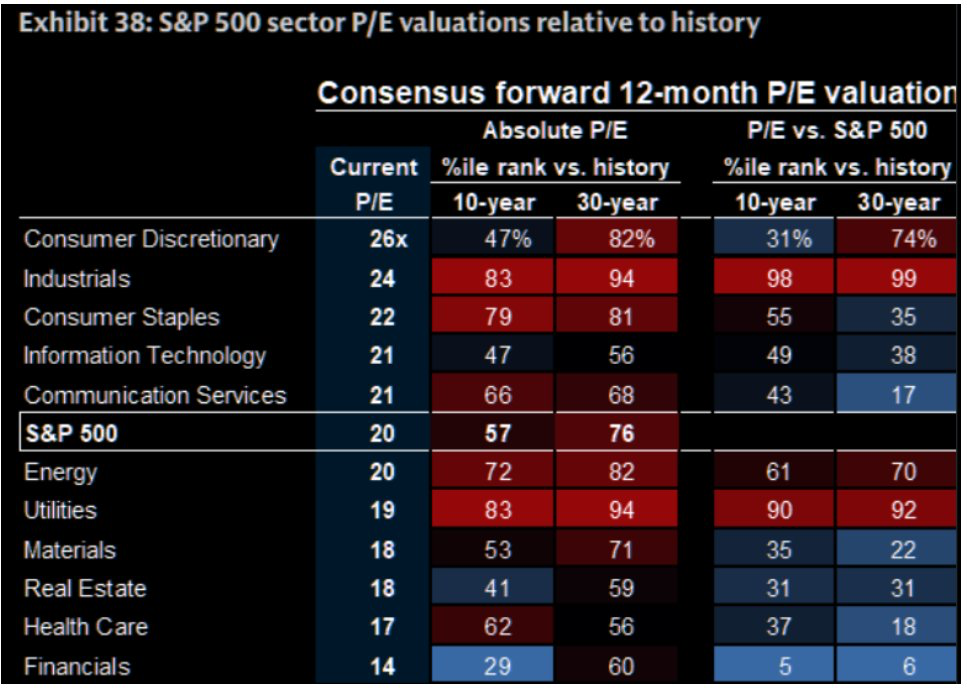

A closer look at the valuation levels of the different industry sectors, shows that Technology and Consumer Discretionary sectors have fallen to very attractive levels relative to the rest of the market’s 10 year valuation.

So long as companies can continue to expand earnings, we think the stock market can hold up against a lot of the uncertainty still to come in Iran.

We expect another period of uncertainty once the ceasefire breaks, US Marines arrive in theater and more clarity about the damage to energy infrastructure leaks out of allied nations. However, history shows that investors should be looking past the current conflict.