This week, the stock market again hit new all-time highs due to strong corporate earnings reports. Since the Iran War began, we’ve been saying that investors would look past the conflict after the initial emotional reaction and refocus on strong earnings reports. But what will happen as earnings season ends?

In the next few weeks, the bulk of earnings reports will be complete, analysts will have adjusted their models, and the markets will look around for a new short-term focus. We think that their focus will again shift back to Iran and the impact that higher oil prices might have on the economy and on Fed Monetary Policy. We won’t be surprised if the early summer months see a spike in volatility.

Oil Prices

The current shipping blockade in the Strait of Hormuz has reduced daily global oil supply by about 10 million barrels per day. Many Asian nations like Japan and South Korea are reaching the end of their oil reserves. If the flow of oil isn’t restored in the next month, the real economic impact of the Iran War could become severe.

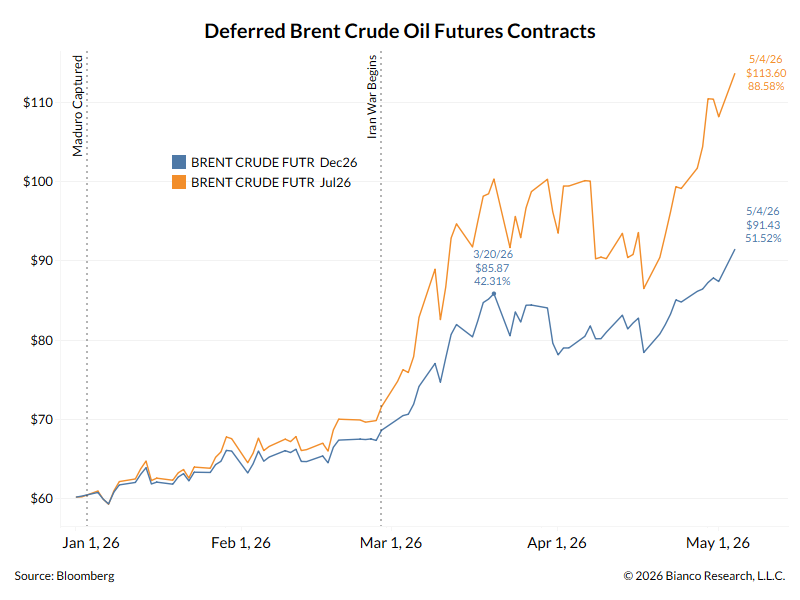

Given that reality, Oil Futures have drifted higher over the last few weeks.

Investors are assuming that we will not have a resolution to the supply issue by July and have pushed July 2026 Brent Oil prices to nearly $114/barrel. This is up 63% from the July 2026 price when the conflict began.

December 2026 Brent Oil contract prices have risen to $91.43/barrel on these same fears. The backwardation of the oil market is slowly disappearing on speculation that the supply constraint may continue longer than expected. Brent Oil price for today closed at $110.50/barrel.

Fed Monetary Policy

As the assumption for a quick restoration of oil supply and lower prices disappears, economists and analyst are being forced to reprice their expectations for inflation and interest rates.

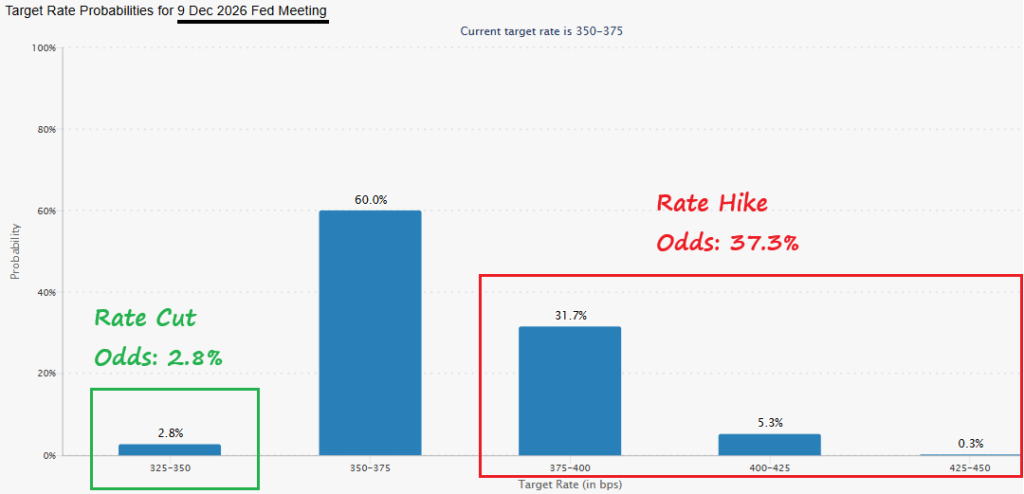

The Fed Funds Futures Market is now pricing in just a 2.8% chance of an additional interest rate cut through December 2026. Most disturbing, is that this market is now predicting a 37.3% chance of the Fed hiking interest rates to combat oil supply related inflation.

Both elevated oil prices and higher than expected interest rates are negatives for short-term stock prices. If investors shift focus from a great earnings season to higher interest rates and inflation, this might push some to de-risk their portfolios.

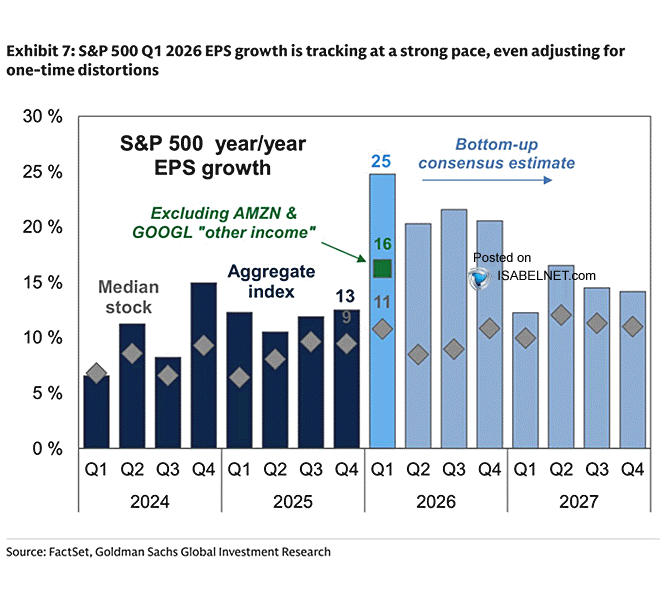

However, we wouldn’t expect this pessimism to last very long. Forward earnings estimates continue to climb and are expected to be very strong over the next few years.

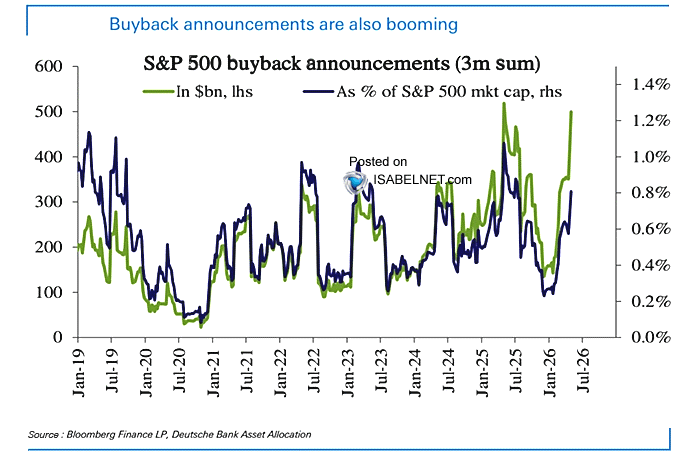

In addition to strong earnings growth, corporations have announced record high stock repurchase programs over the last few months.

We would expect that any short-term fear this summer will get swept away again as earnings are reported after Q2.